In my previous post I discussed how you can earn a lot of free travel quickly by signing up for a credit card with a big sign-up bonus. A question that arises for many people is: what effect does signing up for credit cards have on one’s credit score?

It is an important question. A good credit score is key to getting loans, such as for a home mortgage, at the lowest rate possible. A quarter point swing in the interest rate on a 30-year home loan can easily be the difference in $10,000, $20,000, or even more over the life of the loan.

In most cases it would be foolish to earn credit card bonuses if doing so meant you would miss the lowest rate on a home loan. But does it?

In an effort to answer such questions, I will cover the following topics in this post:

- How credit scores are determined

- The effect that opening credit cards has on credit scores

- How to determine what your credit score is and decide whether you are in a good position to open a credit card

How Credit Scores are Determined

Credit scores communicate your credit worthiness to lenders. They are an important factor in a lender’s determination of whether to lend to you and, if so, on what terms (such as at what interest rate).

The most widely used credit scores are FICO scores, with 90% of lenders using those scores. The three credit bureaus that compile those scores are Equifax, TransUnion, and Experian. Because each bureau records slightly different information about you, your FICO score from each bureau will typically differ somewhat.

These FICO scores range from 300 to 850. The following is a loose approximation of the quality a lender might assign to any given score:

- Excellent Credit: 750+

Good Credit: 700-749

Fair Credit: 650-699

Poor Credit: 600-649

Bad Credit: below 600

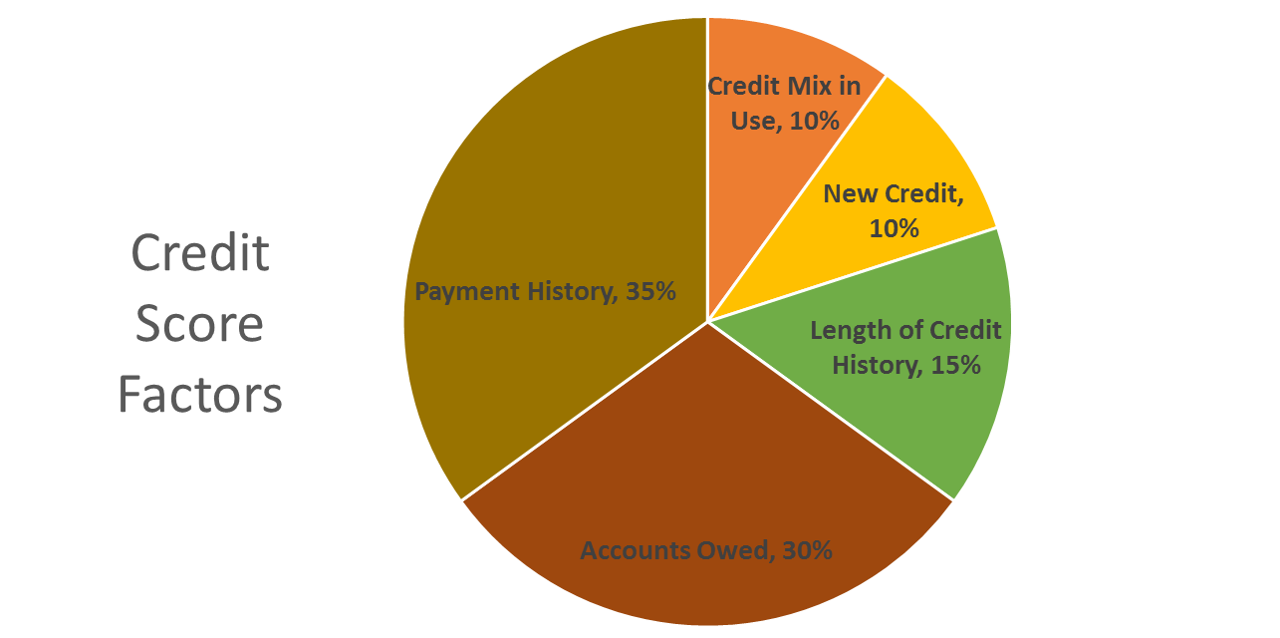

FICO scores are comprised of the following factors. As we’ll see below, they are important to understand from the standpoint of assessing the effect that credit card applications have on your credit score.

Key Components of FICO Score

Here’s a summary of each of the factors that influence your credit score:

- 35% = Payment History: This is the most important factor. You improve this factor by paying your credit card bills and other loans on time.

- 30% = Accounts Owed: This is the second-most important factor. It measures several items, including the total amount you owe across all your accounts, how many of your accounts have balances, etc. Arguably the most important item it measures is your credit utilization ratio, i.e. how much credit you use as a percentage of the total credit available to you. By lowering that ratio, you improve this factor.

- 15% = Length of Credit History: This factor is improved by having a higher average age for your credit accounts as well as by having an long age for your oldest account.

- 10% = Credit Mix in Use: By having a variety of different types of accounts (credit cards, home loans, auto loans, etc.) you can improve this factor.

- 10% = New Credit: Recent “hard inquiries” (inquiries for credit cards or loans) hurt your score. You can improve this factor by avoiding hard inquiries.

The Effect that Opening Credit Cards has on Credit Scores

Opening credit cards typically does not affect two of the above five factors:

- Payment History (35%): As long as you pay off the credit card balance on your new card just as you do on any previous card(s) you have, opening a new card should have no effect on this factor.

- Credit Mix in Use (10%): If you’ve never had a credit card before, opening a card is likely to help this factor of your score. Assuming you already have credit cards, however, the effect of opening a new credit card on this aspect of your score is likely negligible.

Opening a new card does affect the other three above-mentioned factors. That influence has both a short-term and long-term effect on your credit score.

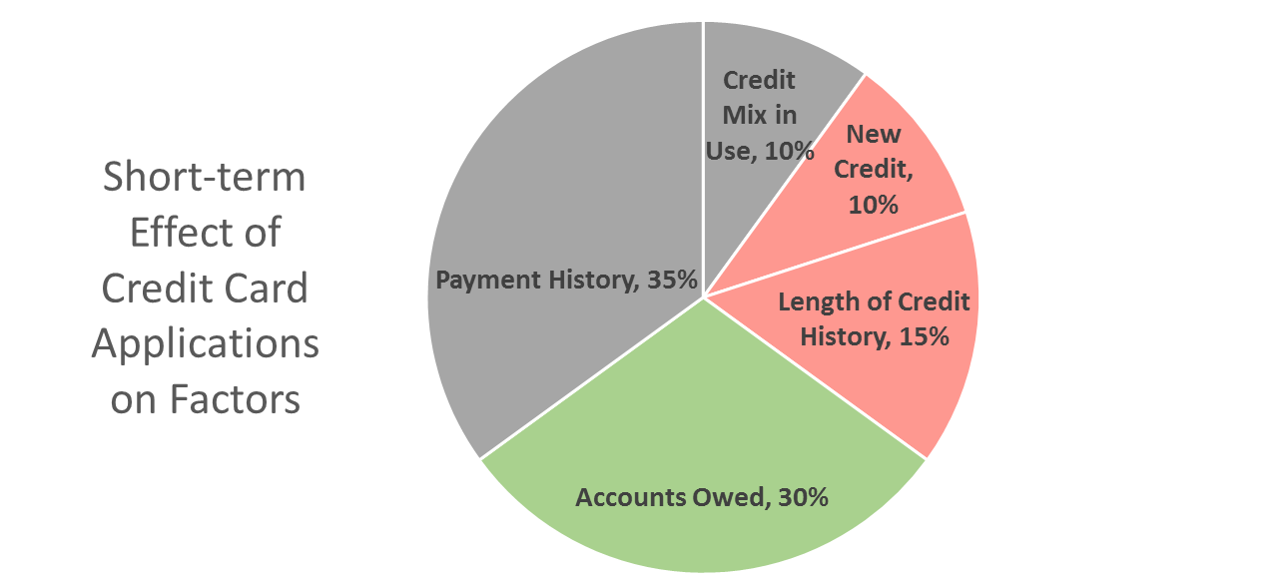

Short-term Effect

The short-term effect of opening a new credit card is, perhaps surprisingly, often minimal. For some folks, their score actually rises. Perhaps more commonly, you may experience a temporary drop in your score of, say, 3-10 points. That has been my personal experience.

The following diagram helps illustrate why opening a new card often has a minimal effect. Green color represents factors that are typically improved by the new card. Red represents factors that are typically harmed by the new card. (Gray indicates factors that are typically not impacted.)

When you open a new credit card, the short-term effect is often influenced in this way:

- Accounts Owed (30%): This factor is usually positively impacted because your credit utilization ratio goes down. That is, you now have more credit available to you, but you aren’t using any more credit than you were before you opened the card.

- Length of Credit History (15%): The new card lowers your average age of accounts, so it hurts your credit score in the short term.

- New Credit (10%): A hard inquiry is typically generated when you apply for a new card, so this factor is negatively impacted.

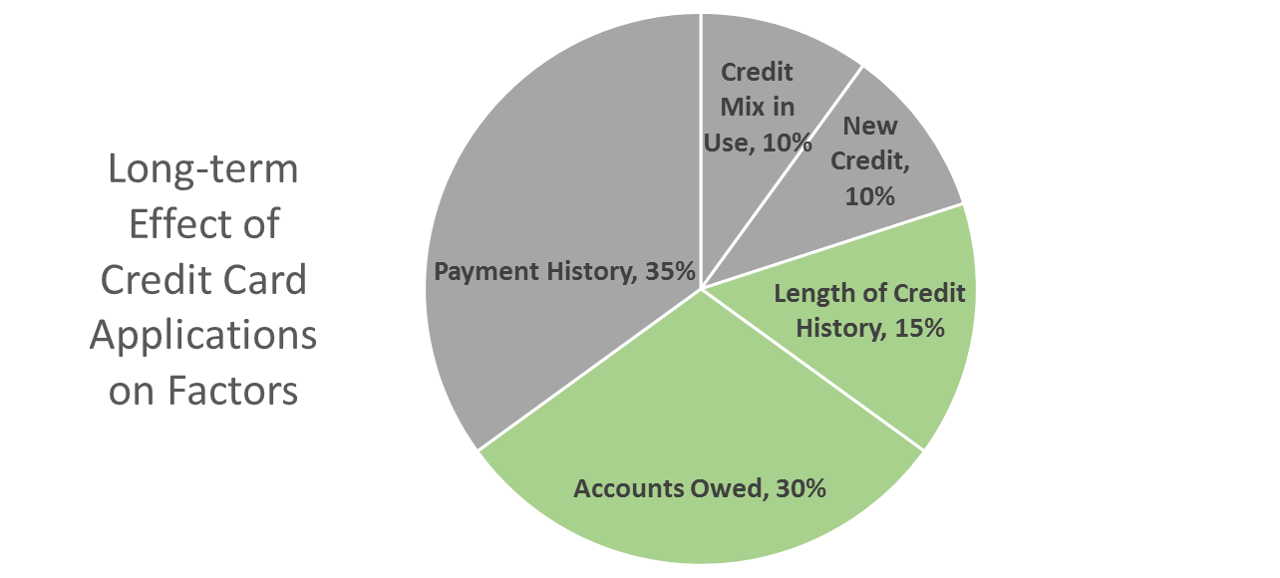

Long-term Effect

The long-term effect of opening a new credit card is almost always positive (as long as you pay it off each month, of course). The following image shows why:

Over time, the impact on your credit score from having opened a new card is almost always positive for these reasons:

- Accounts Owed (30%): This factor is usually positively impacted for the same reason listed in the short-term effect above: lower credit utilization ratio.

- Length of Credit History (15%): Over time, the new card raises rather than lowers your average age of accounts. (Little known fact: even after you cancel a card, it continues to build your average age of accounts for 10 years until it finally drops off your credit reports.)

- New Credit (10%): The short-term, negative impact of the hard inquiry you receive when opening a credit card diminishes and ultimately dies off over time. Some people report their scores bouncing back after 3 or 6 months. Others say that the inquiries have no effect after 1 year. Whatever the case may be (and it likely depends on particular circumstances), the hard inquiries themselves drop off your credit report after 2 years, at which time they couldn’t possibly have any further effect.

How to Determine what Your Credit Score is and Decide Whether You are in a Good Position to Open a Credit Card

To be approved for credit cards that offer big sign-up bonuses, conventional wisdom states that you generally need a score in the 700+ range. That is not a guarantee of approval, but a rule of thumb. Sometimes scores in the low 700s are insufficient, while sometimes scores in the upper 600s are sufficient.

You can get an approximation of your credit score for free via a number of services. A lot of credit card statements now report your score as well. Following are the two services that I use to check my wife’s and my credit scores. Checking your score via these services does not hurt your credit score, by the way (because they are “soft,” not “hard,” inquiries).

- Credit Karma: It provides an approximation of your Equifax and TransUnion scores.

- Credit.com: It provides an approximation of your Experian score.

I would recommend pulling all three scores (Equifax, TransUnion, and Experian) from those two services before deciding if you are in a good position to apply for a new credit card. Ideally all three scores would be above 700, and the higher the better.

Word of Caution for Home Loans

Finally, you may want to hold off on opening credit cards or at least do so at a very modest rate prior to applying for a significant loan such as a home loan.

According to my research, it seems that a credit score of 760 or higher qualifies folks for the best interest rate on a home loan. Scores higher than 760 seem to have no additional positive benefit on the interest rate. By monitoring your credit score, you can avoid applying for a credit card when you fear the short-term effect of doing so will be to lower your credit score below 760.

Even with a score solidly established well above 760, however, mortgage companies may be wary of too many recently-opened credit card accounts on your credit report. For that reason, conventional wisdom holds that the conservative play is to open few to no new credit cards in the 2 years leading up to getting a home loan. Others say you only need to wait 6 months. As is often the case, it probably depends on a number of factors, including what your credit score is, how long you’ve managed credit responsibly, etc.

In my particular case, I applied for very few credit cards in the two years prior to the initial loan on my home, and I got the lowest interest rate possible. Then I opened a bunch of credit cards. Then interest rates dropped, and I decided to refinance in order to try to take advantage of the lower rates. And despite my new credit card accounts, I was still able to get the lowest interest rate possible. So in my case the credit cards didn’t seem to affect the home loan, but mine is just one experience. It’s surely better to be safe than sorry.

Final Thoughts

I hope this post has given you a good understanding of credit scores, why they are important, and how opening credit cards affects them. The overall idea is to reap the benefits of credit cards which I described in my previous two posts while at the same time ensuring that you can qualify for the lowest interest rates possible on big loans like home loans.

This post is the third in the following series:

- Imagining the Possibilities of Free Travel

- Leveraging Credit Card Sign-up Bonuses for Free Travel

- Understanding Credit Scores and the Effect that Credit Card Applications Have on One’s Credit Score (this post)

- Which Credit Cards to Get to Maximize Free Travel

- 5 Creative Ways to Meet the Minimum Spend Requirement in Order to Get the Sign-up Bonus

- How to Use the Miles and Points You Earn

- How to Decide Whether to Keep or Cancel Credit Cards

Question: What questions do you still have about credit scores and the impact that opening credit cards has on them? You can leave a comment by clicking here.

If you liked this post, why not join the 5,000+ subscribers who receive blog updates on how to have more time and money for what matters most? Sign up here.