You just landed at the airport, ready to start your beach vacation. You can’t wait to change your sweaty clothes for a swimsuit. So you head to the car rental agency to grab your car and be on your way. But first, you must make a series of important decisions that you feel completely ill-equipped to make. Do you want collision coverage on the car? What about liability insurance? Seems expensive. But the agent swears you’d be crazy not to purchase the coverage he’s selling.

Your eyes begin to glaze over. You quickly initial here, here, and there. Depending on your decision, you either just forked over a bunch of cash or waived coverage. Either way, one thing is likely: you don’t have good reasons for the decision you made.

I know, because I’m right there with you. Or at least I was until last week.

Over the past week, I’ve done a bunch of research to try to answer the question: When renting a car, should I buy rental car insurance?

Following is the fruit of my research. It will shape whether I accept or decline rental car insurance moving forward.

What does Rental Car Insurance Cover?

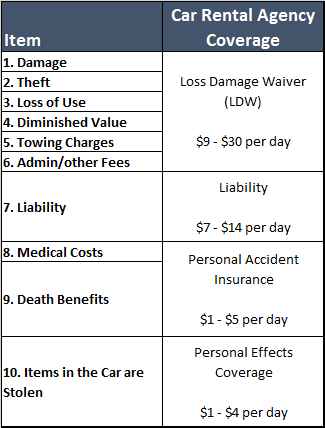

Car rental agencies sell coverage for no fewer than 10 different problems that can arise.

Following are the types of coverage you are likely to be offered at the car rental counter.

Loss Damage Waiver (LDW) [which is Collision Damage Waiver (CDW) plus Theft Coverage]

- Costs $9 – $30 per day

- Typically covers these 6 items:

1. Damage. The vehicle you rent is damaged, by accident or otherwise.

2. Theft. The vehicle you rent is stolen.

3. Loss of Use. You get in an accident. Your rental car gets sent to the shop for repairs. While it is being repaired, the rental agency can’t rent it to others. The rental agency charges you whatever they think they could have made by renting the car during the period of time it was in the shop.

4. Diminished Value. You get in an accident. Your rental car is repaired, but it’s value has decreased because of the accident. The rental agency charges you the difference between what the car was worth before the accident and what it is worth after the accident.

5. Towing Charges. The charges for towing your rental car from the accident to the auto body shop.

6. Admin/other Fees. These are fees for storage, appraisal, claims adjustment, etc. related to the rental car you wrecked.

Liability (a.k.a. Supplementary Liability Insurance or “SLI”)

- Costs $7 – $14 per day

- Covers this item:

7. Liability. This is the cost for damage your rental car does to others’ vehicles or property.

Personal Accident Insurance

- Costs $1 – $5 per day

- Covers these two items:

8. Medical Costs. Such costs include ambulances and medical care for you and your passengers when you get in an accident.

9. Death Benefits. It is a sum (e.g., $175,000) that the rental car agency would pay in the event that you died as a result of an accident in your rental car.

Personal Effects Coverage

- Costs $1 – $4 per day

- Covers:

10. Items in the Car are Stolen. Examples include laptops, GPS devices, etc.

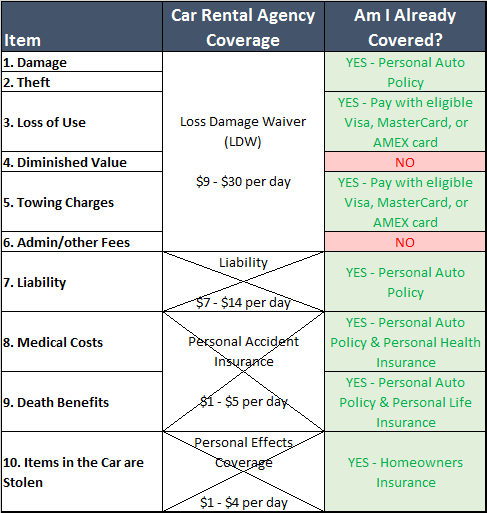

SUMMARY of Coverages Offered by Many Car Rental Agencies

By way of summary, you can often purchase the following coverage at the car rental agency counter:

For maximum protection, you can purchase all the above types of coverage from the rental car agency. But doing so might cost between $21 and $53 per day. That is more than the rental itself might cost, especially if you use the AutoSlash technique I’ve written about. If you drive a rental car just 10 days per year, this is a $200 – $500+ decision.

The question is: Is it possible to get comparable coverage for less money?

And the short answer—at least for many of us—is “yes.”

Important Caveats and Assumptions

In everything I’ve written thus far, and in everything I write below, I can’t stress enough the importance for you to do your own research, consult with your insurance agents, and make your own decisions. The research I’ve done and the decisions I will make based on it are not necessarily what is best for everyone as circumstances can vary greatly. I am not an expert in these matters.

Below I share how I plan to think about rental car insurance given my circumstances, which include:

- My personal auto policy

- Homeowners insurance policy

- Health insurance plan

- Life insurance policy

- The credit card I might use to pay for a rental

Also, in this post I am focused on car rentals with all of the following characteristics:

- Personal (non-business) use

- A “normal” car (not a “specialty” car like a luxury vehicle or a truck)

- Renting in the U.S., not abroad

To the extent that your personal circumstances match mine and your rental has the above characteristics, you might find aspects of the following thought process helpful.

How to Save Money on Rental Car Insurance

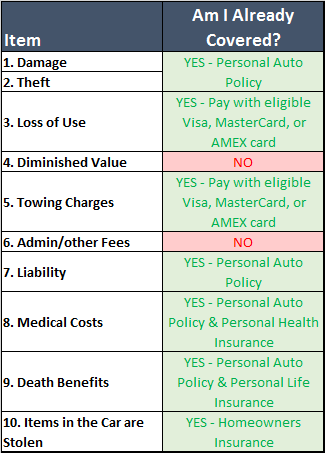

Of the 10 types of expenses that car rental agencies sell coverage for, it turns out that 8 of them are covered for me by other policies/instruments for which I already pay. That’s great news! Here’s how it breaks down.

Personal Auto Policy (PAP)

I have car insurance on the car I own. I spoke with my provider (Geico) about my PAP.

My policy with Geico protects me when driving a rental car as well. Specifically, it covers these items from the above list:

1. Damage

2. Theft

7. Liability

8. Medical Costs

9. Death Benefits

If I were to get in an accident in a rental car while relying on my PAP to cover me, I’d have to pay the deductible for my PAP, and my PAP rates would likely rise following the accident. Were I to rely, instead, on coverage purchased at the rental car counter, I wouldn’t have to pay my PAP’s deductible, and my PAP rates probably wouldn’t rise.

But to my mind, that is not a compelling reason not to rely on my PAP. Yes, I’d have to pay my PAP’s deductible and be subject to rate hikes if I got in an accident in a rental car. But the same is true if I got in an accident in the car I own. If I’m okay with that arrangement for the car I drive every day, I figure I should be okay with it for a rental car as well.

Many Visa, MasterCard, or American Express Cards

If (and only if) you decline the coverage sold at the car rental agency counter, and if you pay in full for the rental with your eligible credit card, many Visa, MasterCard, and AMEX cards cover the following two items from above, which my PAP does not already cover:

3. Loss of Use

5. Towing Charges

(Many credit cards cover Damage and Theft as well, but only if you don’t have a PAP or if your PAP somehow doesn’t cover those items.) Call your credit card company to verify the exact types of coverage it provides.

Personal Heath Insurance

I have personal health insurance. It covers this item from above (also covered by my PAP):

8. Medical Costs

Personal Life Insurance

I have personal life insurance. It covers this item from above (also covered by my PAP) in a robust way:

9. Death Benefits

Renters or Homeowners Insurance

I have homeowners insurance. It covers:

10. Items in the Car are Stolen

SUMMARY of Coverages I Already Have

In summary, by virtue of policies and credit cards that I already have, I am already covered for 8 of the 10 items that car rental agencies want to sell me coverage for:

In a minute I’ll discuss the two items from this list for which I am not already covered.

But for now, it’s worth pointing out that if you have any of the following, you should call the provider to see if, like me, your car rental is already covered for some of the above 10 items:

- Personal auto policy

- Health insurance

- Life insurance

- Homeowners or renters insurance

- A Visa, MasterCard, or AMEX card

My Plan Moving Forward

Because of the coverage I already have, I feel comfortable rejecting 3 out of the 4 types of coverage a car rental agency wants to sell to me: Liability, Personal Accident Insurance, and Personal Effects Coverage. Doing so will save me approximately $9 – $24 per day:

What about coverage for Diminished Value and Admin/other Fees?

The two items for which I am not already covered are:

4. Diminished Value: the difference between what the car was worth before the accident and what it is worth after the accident

6. Admin/other Fees: storage, appraisal, claims adjustment, etc. related to the wrecked rental car

As best I can tell, Admin/other Fees are typically not substantial. They are annoying to have to pay, for sure, but they don’t break the bank.

Diminished Value can be expensive. This article’s author, who is the founder of an insurance commentary site, claims to have seen diminished value charges of as much as $3k, $5k, $7k, and $8k. Although it sounds like those are on the high end of diminished value charges, it would stink to be hit with such a charge.

That said, probably none of us pays for diminished value insurance on our personal car (if there even is such a product). If we get in an accident in our personal car, and our car gets repaired, the value of the car after the accident is less than the value of the car before the accident. It is possible the value of our car could drop by as much as $3k, $5k, $7k, or $8k. Yet we don’t pay to have that loss insured. If we don’t go out of our way to insure against the diminished value of our own vehicle, I don’t see an overly compelling reason to pay for such coverage on a rental car.

No Loss Damage Waiver (LDW) Coverage for Me

All things considered, I, personally, don’t plan to get LDW coverage moving forward. If I needed coverage for all 6 of the items typically covered by LDW, I’d begrudgingly pay the $9 – $30 per day cost of it. I’d know it isn’t a great deal, but I’d bite the bullet.

But if LDW coverage isn’t a great deal when you actually need coverage for all 6 items, I’ve got to think it is a poor value when you only need coverage for these 2 items: Diminished Value and Admin/other Fees.

No Agency-provided Rental Car Coverage for Me

So, moving forward, I don’t plan to buy any kind of rental car insurance from the car rental agency. In fact, I reached this conclusion just before a personal trip to San Diego, and I put my money where my mouth is, so to speak, by not getting rental car insurance on that trip.

Exceptions to the Rule

As I mentioned in the “Important Caveats and Assumptions” section above, there are many exceptions to the foregoing line of thought. It is critical that you consider your own circumstances, do your own research, speak with your own insurance agents, and make your own decisions.

Examples of exceptions that would lead me to a different conclusion include:

- Business Rentals. When renting for business, one’s personal auto policy typically doesn’t provide coverage. For a business rental, I will follow my company’s policy for securing rental car insurance.

- Foreign Rentals. One’s personal auto policy typically doesn’t cover car rentals outside of the U.S. (with the possible exception of Canada). Credit cards are also more restrictive on what coverage they provide for foreign rentals. When renting abroad, I’d dig way into the coverage that my credit card provides for the particular country from which I’m renting. Alternatively, and depending on the country, I’d consider American Express Premium Car Rental Protection (which I’ve used before) or else the coverage offered at RentalCover.com. Finally, I might just purchase coverage from the rental agency as that is typically the safest—even if not always the most economical—bet.

- Specialty Car Types. Many policies and credit cards won’t cover certain car types such as luxury cars, trucks, and other expensive and/or large vehicles. If I were renting any such vehicle, I’d be much more inclined to purchase the coverage sold at the rental agency counter.

Conclusion

Rental car insurance is complicated, important, and no fun. I suspect I have a lot, still, to learn about it. But for now I’ve charted a path that I think will work for most of the cars I’m likely to rent, given my circumstances.

I don’t expect that your situation will be identical to mine. But hopefully the above considerations will allow you to chart a good path forward for yourself as well.

Question: What am I missing from this post? I left some things out to keep from writing a book, but I’m sure there are other salient points that could be discussed. Happy to discuss further in the comments. You can leave a comment by clicking here.

If you liked this post, why not join the 5,000+ subscribers who receive blog updates on how to have more time and money for what matters most? Sign up here.

————

Articles from which I drew information for this post include, especially: